Prime Minister Shinzo Abe held a press conference on October 1 in which he announced the raising of the VAT rate from the current 5% to 8% the following April 2014 as planned. Another hike to 10% was scheduled for October 2015. Did you approve of this VAT hike, or disapprove?

Today, Japan is a country of 100 trillion yen in state spending and 40 trillion yen in tax revenue. The reaction of the majority of the Japanese people is probably this: “In this situation, a VAT hike itself will be unavoidable. However, there are other things that should be done before that.”

I myself have some doubts about the VAT hike.

My first concern is about the use of the money that will be gained by the tax hike.

The VAT hike was supposed to be discussed together with the reforms of the social security system, and the increased tax revenue was supposed to be used to remove people’s concerns about the future. However, the Abe administration is considering a 5 trillion-yen economic policy to supposedly prevent a slump in the economy following the VAT hike. The measures of the policy include “simple payout measures” that provide cash to low income persons, enhancing tax reduction for companies that raise wages, and abolishing the special corporate tax for reconstruction, which was planned to be collected on top of corporate taxes by March 2015, one year ahead of schedule. There was not enough explanation about what happened to the purpose of the tax hike, which was supposed to be meant for social security.

My second concern is that discussions about the problems accompanying the tax hike may have been left behind.

An example is the problem of the difference in value-added tax between Japan and the rest of the world for e-commerce transactions. Value-added taxes are basically imposed on domestic transactions, with importers paying a Value-added tax on imported goods at customs. In the case of electronic books, music, and videos that are distributed through the Internet, however, customs cannot check if consumers downloaded data distributed by business establishments abroad. Japanese companies will lose ground in competition since consumers will be able to purchase electronic books in Japanese and videos made for Japanese people at a price less the amount of VAT if they purchased them from an overseas online distribution service. Unless this problem is fixed, it will affect the employment of 400,000 people in Japan.

I will have substantial concerns if the VAT rate were to be raised without adequate discussions on such matters. It would be fine if a great majority of the people approved of the tax hike, but it would be a significant problem indeed if the great majority felt it was wrong but thought they could not interfere because it was a technical subject. This is because taxes cannot be imposed unless they are legislated based on the consent of the citizens.

Let’s take a look inside the reality of Japan’s tax system, whether or not you intend to pay taxes or have interest in them. Since tax is supposed to be a mirror reflection of a society, any unfair and unreasonable mechanisms existing in society should be reflected in the tax system.

As previously mentioned, the function of taxes is to contribute to the financial resources necessary for the nation we belong to. Nevertheless, why are taxes associated with the impression of something being “stolen” from us?

The history of Japan’s post-war tax system has basically been that of tax reduction on the back of a natural increase in tax revenue due to economic growth. Furthermore, the ruling parties continued to reduce taxes even after the burst of the bubble economy in order to remain in power. They recklessly issued government bonds to maintain tax reductions, sacrificing future tax revenue.

Politicians also behaved as if it were just to reduce taxes. Usually, it is the wealthy class that demands tax reductions. They often claim that they will not demand anything from the state in exchange for not contributing their own money to the state. On the other hand, ordinary citizens are supposed to hope that the government secures public funds by asking the wealthy to shoulder an appropriate burden (i.e., a tax increase) and enhances social security through a redistribution of income. Meanwhile, claims that tax reductions are just have gone unchallenged. As a result of such tax reforms, Japan became a small government with a low tax burden and a low public servant population ratio.

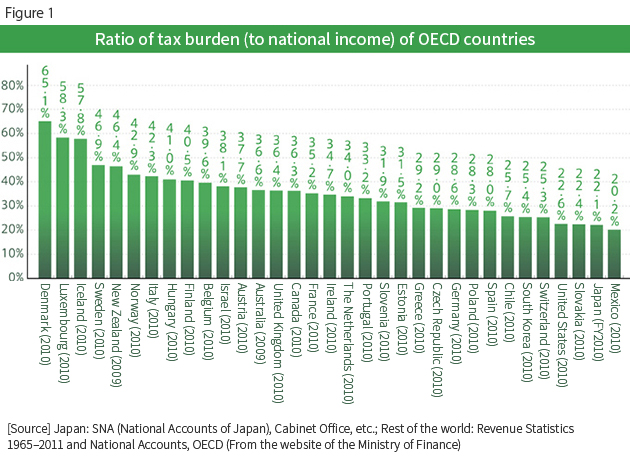

Figure compares the ratio of tax burden to national income of OECD (Organisation for Economic Co-operation and Development) countries. It illustrates that Japan’s tax burden ratio is among the lowest of the majority of developed countries, at 22.1%. The ratio of Sweden, which is famous for its high tax burden, is 46.9%, more than double that of Japan.

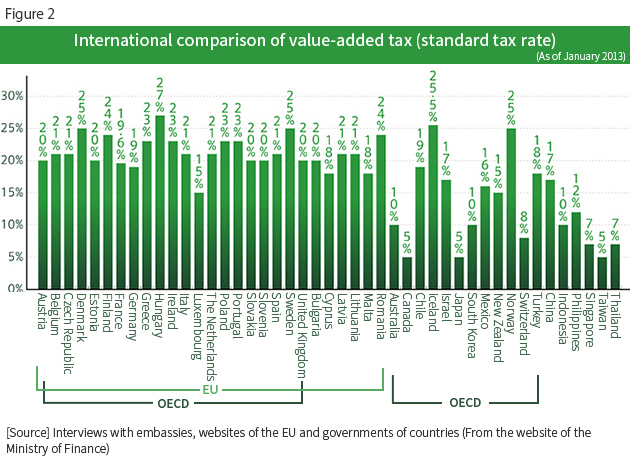

Figure 2 is a comparison of value-added taxes (standard tax rate) between various countries and regions. This also illustrates that Japan’s VAT rate is the lowest, alongside Canada and Taiwan.

Let’s now take a look at the data comparing how people feel about their tax burden. According to the assessment of tax equity in the middle class of different countries carried out in 2006 by the ISSP (International Social Survey Programme), more than 60% of the population in Japan felt that their tax burden was high. This percentage was the fifth highest among the major countries, with Sweden ranking below Japan at eighth.

Japanese people feel as if they’re heavily taxed eventhough their tax burden is low. In contrast, Swedish people do not feel as if they are heavily taxed eventhough their tax rate is high. Where does this difference come from?

Probably there are many opportunities for people in Scandinavia to feel the advantages of their tax burden, while in Japan there are few. This difference is reflected in whether people feel that their taxes are “entrusted to the government” or that they are “stolen by the government.”

Consequently, what should be done to make us feel that taxes in Japan are also entrusted to the government?

First of all, the process of tax reform must be appropriate and fair.

Currently, the process of tax reform carried out each year involves government ministries and agencies presenting their requests for tax reform around August, which are then examined by the tax system research commission of the ruling party and the Tax Commission of the government before being presented as an outline of tax reform in mid-December. Under the administration of the Liberal Democratic Party (LDP), tax reforms are substantially deliberated upon and decided on by the LDP Research Commission on the Tax System. However, the process of the debates by the Commission is completely opaque, sometimes brought to light only in a government outline. A tax reform bill is then prepared and deliberated upon at the National Diet from January to around March, after which, if the bill is adopted and established, a new tax code is applied.

If this process becomes appropriate and fair, the irrationality of the tax system will also be corrected. What is most necessary in doing so is for the members of the Diet and political parties to have a proper understanding and exchange of opinions on tax laws. If the ruling party and their legislators share proper knowledge and create a fair tax reform proposal, the Ministry of Finance would have to comply with it.

It is also necessary for citizens to participate in the process of tax reforms.

I personally am skeptical about whether or not it is really necessary to reform the tax system each year like is done at the present. What about making tax reforms a major national event that takes place once every two years? The government could present a proposal in the first year, while in the second year political parties could engage in heated debates over the proposal. At the same time, all classes of the population could present their opinions on the discussions of the parties.

This would encourage the general public to be more interested in taxes and make them a part of their everyday conversation. To do so, it would also be necessary to develop a system for “visualizing” the details of taxes.

People should also participate more in the discussion of what taxes should be used for. This might enable them to feel that taxes are not something that is “stolen from them by the government” but are “entrusted to the government.” Which tax should be used for which policy would be of interest to the public. Politics is the process of determining this. In other words, tax issues are the very essence of politics.

The oldest records on taxes in Japan date back to around the third century. The Gishiwajinden, which is a history book of old China, includes the oldest mention of taxes in Japan, describing that people paid taxes in the Yamatai Kingdom that was ruled by Queen Himiko.

Taxes have such a long history, but in fact, the majority of their history is a history of times under the rule of kings. In those days, the kings granted chartered powers to administrative institutions to collect taxes from the people. Under such a system, taxes were, from the perspective of the people, merely something that was “stolen” or “seized.”

After WWII, a new constitution was created in Japan, granting sovereign power to the people themselves. A system was put in place where the people ran an organization that was their own “nation” by themselves. Since the taxpayers namely the people, gained sovereign power, they themselves should have set up the tax system. However, tax administration maintained by various systems throughout history such as under the rule of kings who often continued to be adopted an attitude of control.

As for individual income taxes for instance, Japan has become a society where ordinary “salaryman” households hardly have to think about them because they withheld from their payroll. Moreover, their companies carry out year-end adjustments for them as well. This may have fostered the idea among people and politicians that tax increases are evil and tax reductions are just. It is about time that this idea was changed.

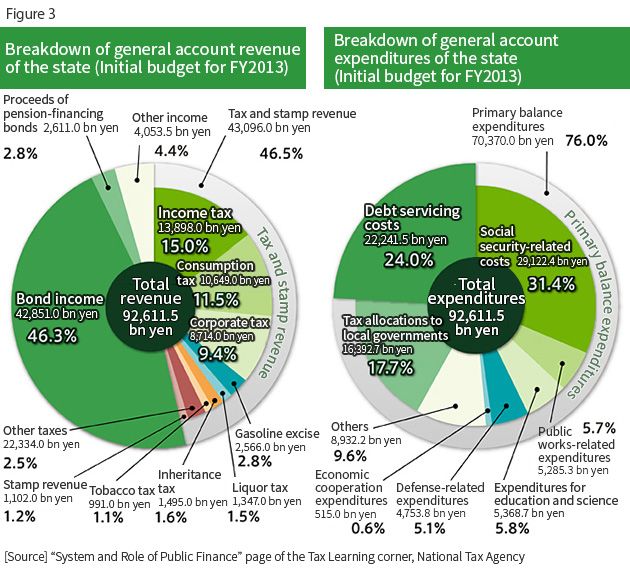

However, do we, Japanese citizens, really understand this? If we still feel that taxes are “stolen” from us, where does this falsehood come from? Japan has become a country of 100 trillion yen in state spending and 40 trillion yen in tax revenue (Figure 3) as a result of the failure of people to confront taxes with an awareness that they have gained becoming a sovereign power. Who is responsible for this?

As long as we have sovereign power, we cannot get away with saying that we neither intend to pay taxes nor have interest in them. It is we who should decide taxes. Let’s take this opportunity with the VAT hike to think about how to reform our tax system and how to use the tax money appropriately.

(This column is as of 2013.)