“I will strive to regain a strong economy with determined commitment.”

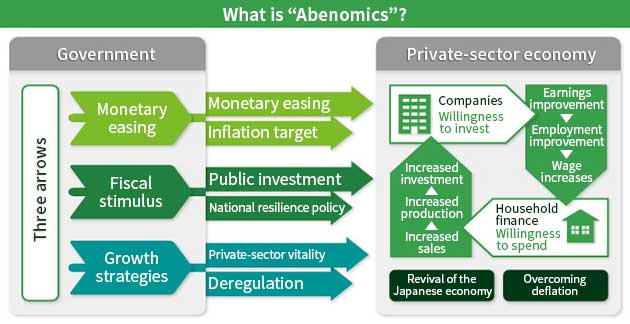

These are the words of Shinzo Abe, the 96th Prime Minister of Japan, during his policy speech at the National Diet. Mr. Abe, who was elected to his second term as prime minister after the Liberal Democratic Party regained power from the Democratic Party, which ruled for approximately three years, announced his policy of promoting economic revival with the “three arrows” of monetary easing, fiscal stimulus, and growth strategies. You must be seeing and hearing the term “Abenomics,” a portmanteau of “Abe,” of Prime Minister Abe, and “economics,” almost every day.

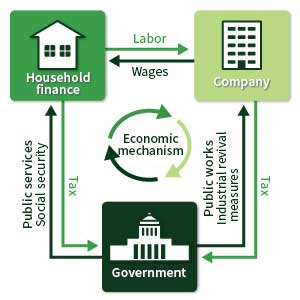

To begin with, the economy refers to the flow of money, goods, and services. People work in companies to create goods and services. The companies pay those people a salary (money). The people buy goods and services from companies. The government receives payment of tax (money) and distributes public services such as the police system, pensions, and allowances to the people. The economy is the flow of all such transactions involving money that are necessary for people to lead their lives.

A “good economy” refers to a state where money circulates rapidly with momentum among households, companies, and the government. If the economy is good, households will spend more money on shopping, companies will generate more profits and pay higher salaries to employees, and the government will earn more tax and run the country better. On the other hand, a “bad economy” refers to a state where there is no momentum in the flow of money. This is exactly the state the Japanese economy is in today.

A deflationary phenomenon has been lingering in the Japanese economy. Deflation means that prices drop continuously due to the lack of sales of goods and services. It may seem like a good phenomenon at first glance, but if goods and services do not sell unless the prices go down, the salaries of the people working there will drop, leading to payroll cuts and job losses. Since household income drops due to lower salaries, people will stop buying. This will lead to a further drop in the sales of goods and services. This deflationary phenomenon is said to be behind the sluggish Japanese economy of recent years.

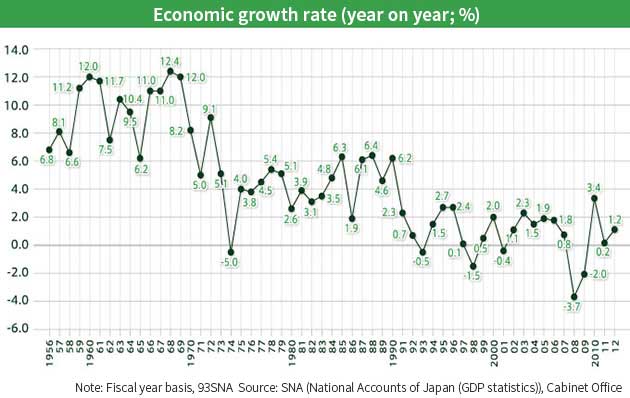

The growth of an economy is indicated by GDP (Gross Domestic Product). GDP is the sum of the monetary value of products and services newly produced in a country over the past year, while the economic growth rate is the rate of growth of GDP from the previous year. When the economy is good, the GDP growth rate will be higher, and when it is bad, it will be lower.

Take a look at the chart above. Japan experienced high economic growth after the end of WWII, with the growth rate averaging 9.1% between 1956 and 1973 and 4.2% between 1974, after the oil shock, and 1990, when the bubble economy started to burst. In contrast, since the bubble burst in 1990, the growth rate has remained sluggish until fiscal 2012, averaging 0.8%. This period is also called “the lost two decades.”

During the oil shock (which caused global economic turmoil due to a surge in oil prices) of the 1970s, the Japanese economy plunged to negative growth for the first time since the end of the war. Article 4 of the Public Finance Act stipulates that state spending shall be financed from revenues other than public debt and borrowings, which means that government bonds cannot be issued to cover the country’s deficit. However, a special law was enforced at the time to enable deficit-covering government bonds to be issued over the short term, and such bonds were issued to support the Japanese economy.

Subsequently, Japan was called “Japan as No. 1” due to the growth of the automobile and electronic products industries. Although exports had increased at the time to a level that caused trade frictions, the government ran the Japanese economy by supplementing budget shortages with deficit-covering bonds. Japan’s total debt amounted to 991 trillion yen at the end of fiscal 2012 and is expected to exceed 1,000 trillion yen by the end of the current fiscal year. Under such circumstances, Japan’s finances may collapse as the finances of some European countries almost did. What should be done for the Japanese economy to overcome this slump and regain a strong economy?

“Fiscal stimulus” is for the government to step directly into private markets and spend money. Meanwhile, “monetary easing” is to provide money from an indirect supporting position, expecting the private markets to make good use of the money if the supply of money increases in the market.

The conventional and orthodox methods of fiscal stimulus were either tax reduction or public works, while those for monetary easing were the reduction of the official discount rate by the BOJ or “buying operations,” in which the BOJ increases money in the private markets by purchasing government bonds in the private markets and paying for them.

The previous Japanese economy can be compared to a condition where you think you caught a cold and took medicine or received a drip but the cold was not cured and lingered on until you developed a case of pneumonia.

If it was a human body, you would first take some medicine, treat the cold, and recover from it. After your body has recovered, you would exercise or change your lifestyle to build up your health and try to maintain it.

It’s easy to understand if you think the same with the Japanese economy. First, treat the condition with fiscal stimulus and monetary easing as drugs or injections, recover health to normal condition, revive industries with growth strategies, and improve the strength and health of the Japanese economy. This is what Abenomics aims to do.

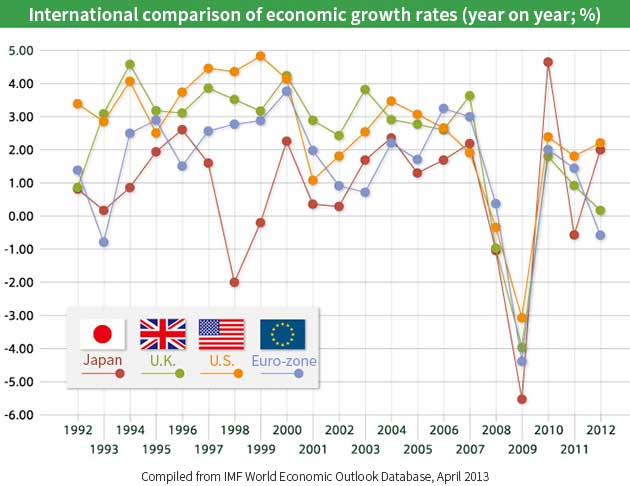

The 1980s was a period of economic transformation for Europe and the United States. The U.S. economy hit the bottom due to the Vietnam War, while the U.K. suffered from the so-called “British disease” and was overtaken by other countries after being at the top since the industrial revolution in the 18th century, ultimately finding itself the most out-of-date. Both countries faced the need for economic revival.

Britain’s Thatcher administration created a small government by improving efficiency through the privatization of state-owned companies and reduction of excessive welfare. The U.S.’ Reagan administration revived U.S. industries by invigorating private companies through bold deregulation and liberalization. Companies born around this time that later grew to become global firms include Apple and Microsoft. These economic revivals of the U.S. and the U.K. succeeded, enabling them to maintain some of the most stable growth rates among developed nations with 2–3% on average since the 1990s up to now.

Then, what about Japan? As I mentioned earlier, Japan’s growth rate experienced greater fluctuation than in other developed nations in Europe and the United States, and averaged 0.8% over the past 20 years. Japan also privatized state-owned corporations, with Nippon Telegraph and Telephone Public Corporation becoming Nippon Telegraph and Telephone Corporation (NTT) in 1985, the Japanese National Railways becoming Japan Railways (JR) in 1987, and the Japan Post becoming Japan Post Co., Ltd. In 2007. Deregulation or liberalization of related laws upon privatization allowed new companies to enter the market, prices to drop due to competition between companies, various services to be created, and new employment to be generated.

However, if we look at how the U.K. and the U.S. economies recovered since the 1990s, there are still many things Japan has not done, which suggests that there is still considerable potential for Japanese industries.

One example is electric power. Although Japan’s electricity companies have been privatized, they are protected by the law and enjoy a monopoly. If a private company produced electric power, it will not be allowed to borrow power cables, without which it cannot supply electricity and hence cannot do business. However, if, like the current NTT, it will be able to use power cables by paying a usage fee or if a company that generated electricity can sell electricity to Tokyo Electric Power Company, it will lead to greater business opportunities.

If the flow in which the Nippon Telegraph and Telephone Public Corporation was privatized and became NTT, which led to the development of large companies like SoftBank and au and vitalized the IT industry, leads to genres that have the potential for business development in the future, such as energy, ecology, environmental issues, and social welfare, it might give birth to many derivative industries.

However, the reality of Japan today is that it is difficult for private companies to enter certain areas since there are quite a few areas protected by the law as they are considered sanctuaries or to be of national interest. Deregulating or liberalizing such regulations will vitalize various industries, enabling Japan to target economic growth of 2%. Of the three arrows of Abenomics, the growth strategies hold the key.

Abenomics has only just begun. Since the start of the Abe administration, the yen, which had been trading at around 80 yen to the dollar, has depreciated to more than 100 yen to the dollar, while stock prices have hit a new high for the year to the 15,000 yen-level. These maybe signs of an economic recovery.

However, companies that import resources and foodstuff to make products or companies that sell imported goods are forced to raise prices due to the rapid depreciation of the yen. Moreover, there have been concerns over the market’s oversensitivity or unstable conditions as evidenced by the recent violent fluctuations of the yen and share prices, as well as sensitivity toward the U.S. economy.

We, the citizens, are suffering a huge blow to our household finances since the improved economy has not yet led to greater income. When will the day come when citizens can really feel that the economy is good, and will Japan really be able to overcome deflation? At the moment, it’s undeniable that there are concerns toward the future.

However, let’s change our perspective a little.

Although a natural resource called methane hydrate has been found in Japan recently, the lack of such natural resources has had a large impact on the Japanese economy. However, the Japanese economy managed to grow by leaps and bounds during the 1960s and entered a period of rapid growth. It is said that this was due to the high quality of the Japanese workforce. The Japanese deserve to be proud of themselves for their high potential, such as in their world-class energy-saving technologies, which developed in the 1980s, as well as their manufacturing technologies and technology development skills.

I think Japan is extremely resource-rich if you consider people’s potential and technological capabilities to be resources as well. Due to the growth strategies of Abenomics, we might see the birth of new industries or many new entrant companies. The efforts of students as well as those who are working to improve themselves in order to carry out better economic activities in the future Japanese society may become Japan’s potential. The savior of the Japanese economy might actually be each and every citizen.

(This column is as of 2013.)