![]()

私たちが生きている世界には、

身近なことから人類全体に関わることまで、

さまざまな問題が溢れています。

意外に知られていない現状や真相を、

本学が誇る教員たちが興味深い視点から

解き明かします。

皆さんは、「ふるさと納税」という言葉を聞いたことがあるでしょうか?

ふるさと納税とは、任意の自治体に2,000円を超える寄付をすると、個人住民税や所得税が控除される制度のこと。元々は2008年、第1次安倍政権のときに、税収の地方間格差や、過疎などによる税収減少に悩む自治体に対して、格差是正を推進するための新構想として創設された制度です。2011年の東日本大震災の際には「被災地を支援したい」と多くの人たちが寄付を行い、前年比で約10倍となる649億1,490万円が集まりました。

最近では、テレビや雑誌などでもさかんに紹介されていますから、「ふるさと納税」という言葉を耳にする機会は増えましたが、詳しくは知らないという人も多いのではないでしょうか。

では、この「ふるさと納税」制度について、その特徴を簡単に紹介しておきましょう。

まず、名称に「納税」とありますが、実は寄付金控除の一種です。全国の任意の地方自治体(都道府県・市区町村)に対し、個人が2,000円を超える寄付を行うと、住民税と所得税から一定の控除を受けることができる制度です。つまり実質的に、いま納めている県民税・市民税の一部を、寄付先の自治体へと移転することになります。

「ふるさと」と名付けられていますが、自分の出身地や居住地である必要はなく、自分が応援したいと思う自治体へ自由に寄付を行うことができます。また、多くの自治体では、寄付金の使い道が選べるようになっています。例えば、東日本大震災の時に多くの人が行った「復興支援のため」のほか、「大学時代に住んでいた自治体の自然環境を守りたい」「ふるさとの伝統・文化を守り育てたい」など、自分が共感する政策やイベントなどに対して寄付をすることも可能です。

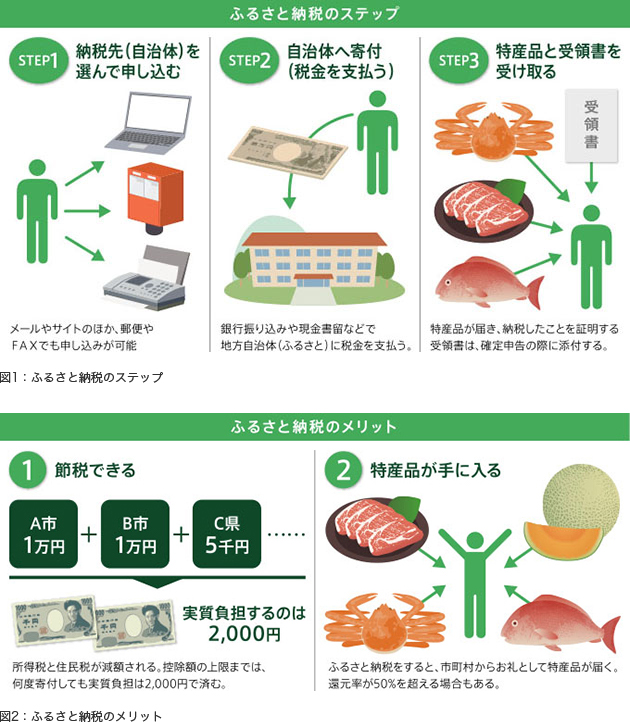

そして、ふるさと納税を行った(寄付をした)人に対して、地域の特産品や民芸品などの特典を用意している自治体も数多くあります。自分の欲しい特産品のある市や村などに寄付をするのは、ふるさと納税の大きな魅力です。(図1・図2)

平成25年度課税(2012年に行われた寄付が対象)においては、東日本大震災前の年度よりもふるさと納税の寄付は増加しており、こうした特産品などの人気で、ここ1~2年はさらに増加していると考えられます。こうした人気を背景に、「地方創生」を重要課題に掲げる安倍政権は、今年度ふるさと納税の控除額の上限を引き上げ、制度を拡充しました。

このように、さまざまな特徴や多くのメリットがある「ふるさと納税」ですが、「地方間格差や過疎などによる税収の減少の解消」「自分が生まれ育った地域やお世話になった地域を応援したい」という本来の趣旨からしだいに逸脱し、特に最近では、高額な寄付を行った人に対して「牛一頭を贈呈」する自治体も出てくるなど、“自治体間の特産品競争”が過熱している感もあります。たしかに、寄付金を受ける自治体にとっては、贈呈する特産品のコストや事務関係の費用をかけても、それ以上の「ふるさと納税」があれば、自治体の知名度も上がり、十分メリットがあるということかもしれません。しかし、本当にこれでよいのでしょうか?

ここで、地方税の本質について考えてみましょう。

税には「国税」と「地方税」があることはご存知かと思います。このうち、国税は「応能原則」の考え方に基づいています。応能原則とは、納税義務者の経済的能力に応じた課税がなされるべきであるとする考え方のことです。このため、所得や資産が多い人ほど負担率はより大きくなり、その結果として「所得再配分機能」が期待されることとなります。累進課税の仕組みも、この考え方を実現するものとして組み立てられています。

これに対して地方税は、「応益原則」の考え方に基づいています。応益原則とは、国や地方自治体の提供する行政サービスの受益の大きさに応じて税負担をすべきであるという原則。つまり、「税金は行政サービスを購入するための料金」という考え方です。当然、同じ行政サービスについて支払う税額は、所得や資産に関わらず同じということになります。地方税の場合、提供するサービスが地域的に限定されているため、受益と負担の関係が見えやすいことなどから、「応益原則」の考え方に基づいているのです。

この「受益と負担」という地方税の原則に照らしてみると、「ふるさと納税」という制度に潜む問題点が浮かび上がってきます。

先にも述べたように、地方税は、その課税根拠として「自治体が提供する行政サービスの対価として負担する」という性格を持っています。これに対して、ふるさと納税をする人は住民税が控除されますから、行政サービスを受けていない自治体に税(実際は寄付金)を納める一方で、いま住んでいる地域の自治体に対しては、「行政サービスは受けながらも、負担すべき税の一部しか納めない」ことになります。多くの住民が「ふるさと納税」を行うようになった結果、現居住地の自治体の税収が減れば、その自治体は、行政サービスの水準を低下させるか、行政サービスの水準を維持するために他の財源を調達しなければなりません。当然、増税という選択肢もありうるでしょう。制度的にはもう少し複雑で、減った税収の75%は交付税で手当てされるため、影響は緩和されますが、交付税を受け取っていない都市を中心とした不交付団体などでは、こういう問題に直面することになります。

こうした事態は、住民税の全額を現居住地に納めている(ふるさと納税を行っていない)納税者にとっては明らかに不利益となります。そして、こうした不利益が、他人の意思によって一方的に生じてしまうということは、「受益に応じた負担」という地方税の理念の根本を揺るがす問題であると言わざるを得ません。

私自身は、「ふるさと納税」が「地方間格差や過疎などによる税収の減少の解消」や「自分が生まれ育った地域やお世話になった地域を応援したい」という本来の趣旨の範囲内で行われている限りは、地場産業の育成や振興に寄与することもあり、好ましいと考えています。実際に、地方で育った若者の多くが進学・就職を機に都会へ出ていってしまうという問題は深刻です。教育などに要する費用を負担しても、優れた人材は都市に流出してしまい、その結果、都市部の自治体の税収は潤い、人材を育んだ地方自治体の税収は減少する……これは、地方にとっては悩ましい事態です。県外へ出て行った人たちに、ふるさと納税を利用して「出世払い」をしてほしいと願う気持ちも十分に理解できます。

しかし、寄付が集まらず、控除額だけがかさんでいく大都市が、その強大な財政力を背景に、本気で「ふるさと納税」のサービス競争に参入し始めたらどうなるでしょうか? 地方自治体に寄付をするメリットが減り、都市と地方の格差がさらに拡大する可能性も否定できません。特産品の豪華さで寄付を一時的に増やしても、それが持続可能なものであるかどうかは疑問です。

メディアには「節税対策におすすめ!」「コストパフォーマンスが高いお得な自治体をランキングで掲載!」など、豪華な特典にフォーカスした情報があふれています。しかし、こうした傾向が過熱すれば、結局は善意の納税者が不利益をこうむることになるのです。

「自分を育ててくれたふるさとのために貢献したい」という思いから始まった、せっかくの「ふるさと納税」制度。節度をわきまえた運用によって、本来の趣旨が損なわれることなく持続的な制度となるよう願っています。

(2015年掲載)